Nonprofits are in distress. Can a private equity model save them?

Nonprofits are in distress. Can a private equity model save them?

Hello. Welcome back to Interior Analytics, a newsletter about the business of American nature. Today I write about the distressed state of nonprofits and how certain principles of private equity can help them. If you like what you see, please give it a like, share or reach out on twitter @sambarkley_

This post has been on my ‘shelf’ for quite some time. With the pandemic threatening so many great organizations, including those doing the much needed work in climate change and conservation, I felt it was time to dust off this concept and put it out there.

If this is your first time here, poke a round a little and consider subscribing to have this kind of stuff dropped into your email every now and again.

Enjoy!

Sam

Photo by the blowup on Unsplash

Nonprofits are in distress - Can a private equity model save them?

Private equity and Philanthropy are disparate — but can they learn from each other?

Nonprofits are struggling but the opportunity for impact is massive

Generosity needs to get aggressive

Measurement is key

Many nonprofits will not survive the pandemic. Several have already closed, others hang on by a thread and the rest are forecasting six to twelve very challenging months as the looming effects of a sluggish economy start to take effect.

90% of organizations experienced revenue loss in 2020.

69% applied for a Paycheck Protection Program Loan ranging between $5K and $6.8M. Fewer than half have received funding.

64% reported cutting back on programs, while 48.8% ceased a primary program.

Sources: Charity Navigator, Reuters, La Piana Consulting

Like any business, nonprofits that were struggling pre-pandemic have been put through the ultimate stress test. Whatever existing issues there were have been compounded by a virus that shut down most if not all revenue streams, sidelined frontline fundraisers from travel and revealed cracks in their once reliable donor base.

Private equity funds, through aggressive sourcing and complex financing, invest in distressed companies with potential. Eventually, they sell these reorganized assets and return a profit to their investors.

Can philanthropy deploy these same principles to their investments? What might it look like?

A nonprofit should be able to seek a similar partner. Bringing the benefits of expert guidance, efficiencies and capital to their organization. Making sure that the societal problem they are solving receives the necessary tools to extend, measure and grow the impact of their mission. Also known as: the return on philanthropic investment.

This isn’t an entirely new concept. Venture philanthropy firms like New Profit and Draper Richards Kaplan have been adopting a similar venture capital model for several years and to much success. But they typically look to ignite an early-stage idea or solution rather than rescue or restructure an organization.

PE style instruments, like the leveraged buyout (LBO) model of investing, could unlock the greatest social and environmental outcomes of a generation.

This would close the gap between maximum impact and (in some cases) the catastrophic dissolution of these vital services.

But first things first, we need a new name for LBO.

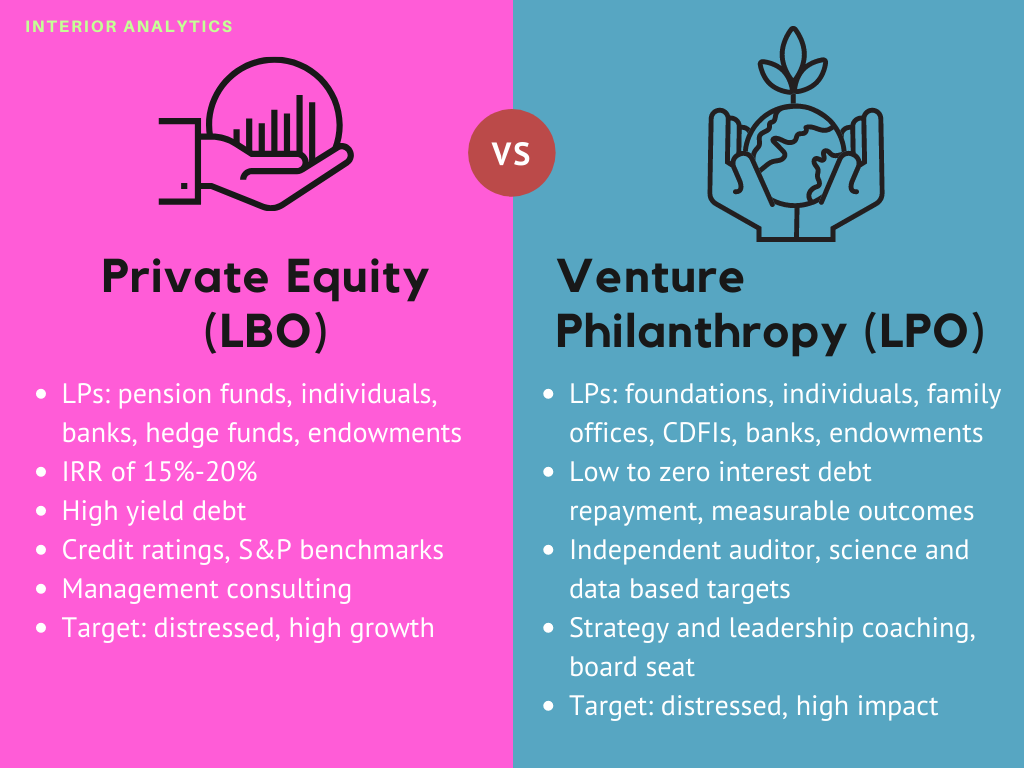

A closer look at PE and philanthropy as investment vehicles are, on the surface, completely in conflict with one another. Private equity is designed to return a consistent profit to investors and philanthropy is an attempt to solve a societal issue with no monetary expectation in return (except tax incentives). One is measured in the simplest of terms: internal rate of return (IRR) i.e. money, the other is measured more vaguely by societal impact and outcomes.

The sausage might get made with different ingredients but the products are essentially the same. In the end, the crux is the LPs taste e.g. the expected rate of return.

I am not suggesting large foundations or innovative philanthropists go on a shopping spree for cheap impact. *well maybe that’s exactly what I am saying* And it is likely illegal to collateralize an organization’s assets in exchange for a donation (whether a modified loan or not). But, in theory, these distressed nonprofits desperately need debt restructuring, an infusion of operating capital, help with organizational strategy and tools to measure their impact for a clear path to growth.

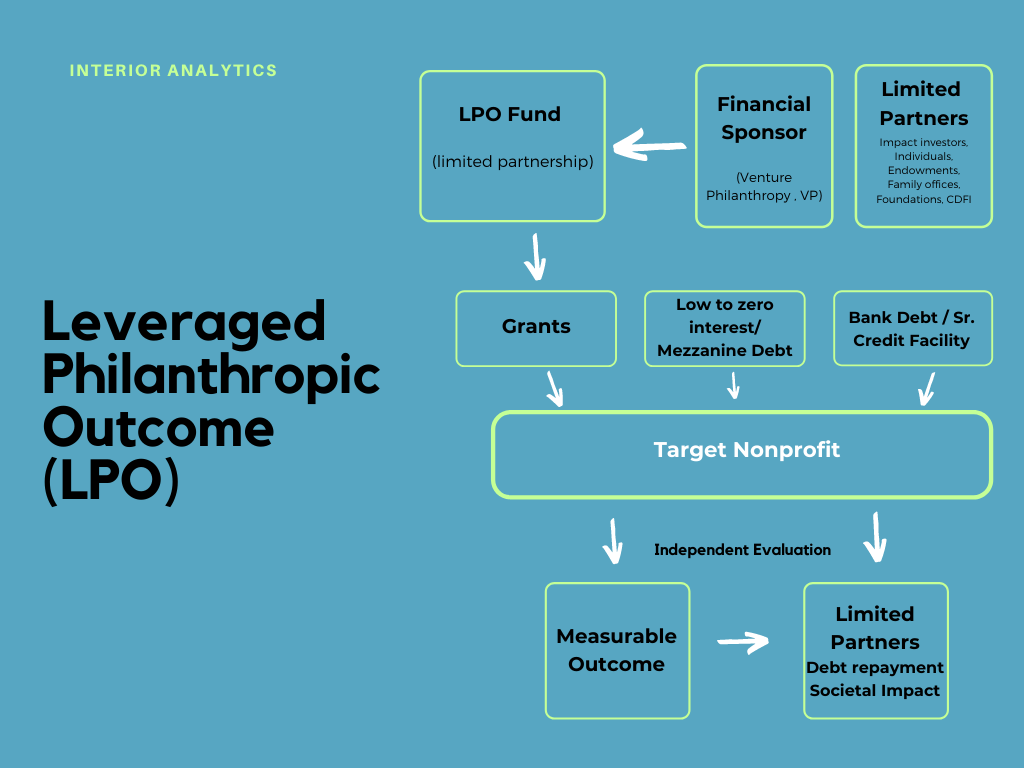

Let’s call it: Leveraged philanthropic outcome (LPO)

I explore applying the principles of private equity to the distressed state of nonprofits and reframe the leveraged buyout (LBO) to a leveraged philanthropic outcome (LPO). Also, I take into consideration the incentives for a private equity investor versus a philanthropic equity investor; the existing financial tools available, and the current market opportunity that exists for venture philanthropy. Spoiler: It’s massive.

The problem and the opportunity

According to the National Council on Nonprofits there were 1.4 million organizations, spending $2 trillion annually and employing 10% of the total US workforce before the pandemic hit. A quick glance at the fallout over the last 9 months reveals a staggering 83% of nonprofits reporting a reduction in revenue, (some states seeing 50%-70% drops), a 47% reduction in force and 92% are seeking loan assistance.

As John Mcintosh from SeaChange Capital wrote in a recent column:

Covid-19 is poised to become an extinction-level event for America's nonprofits.

Many trade organizations and state level nonprofit associations have released surveys of their members, each showing grim forecasts for the organizations operating in their area.

A closer look at Minnesota in particular reveals what the potential fallout of a mass closure event would mean. Not only do these nonprofits provide critical services, but their economic impact is huge. Over 9,000 nonprofits operating in the state employ 13.3% of the overall workforce. The Minnesota Council on Nonprofits also report a $1B loss in nonprofit revenue across the sector -- and almost half of those organizations have less than a month to three months of operating capital in the bank to survive.

Macintosh adds:

The truth is that our capitalist system will likely quickly rebuild the for-profit ecosystem after the Covid-19 crisis has passed. Planes will fly. Cruise ships will sail. New restaurants will emerge to take the place of those that failed, buying the fixed assets at a discount, occupying the same storefronts at lower rents and serving the same clientele.

Adaptation may be a hallmark of the most successful and enduring companies, but it is not a strength of most nonprofits.

Pivoting away from your mission to claim short-term revenue, while a means to survive, is in most cases non-negotiable. Meanwhile, as operating and overhead costs increase, most donations are restricted, going only to very specific needs or functions that support mission-related projects. Additionally most philanthropists clearly define that no portion of their donation be designated for administrative fees (operating costs).

I can hear the screams of my PE and philanthropy friends seething at my oversimplification of these models. My disclaimer is this: capitalism and philanthropy are at odds, this is clear. But why can’t we apply each of their own useful tools to solve very similar problems?

The Private Equity Model (simplified)

Private equity begins as a pool of money (fund), gathered by general partners (GP) with a specific investment goal and targeted industry in mind. The GPs raise the fund through limited partner (LP) investors: high-net worth individuals (accredited investors), institutional and pension funds and endowments (among others). There are a variety of ways a fund might make an investment, the most popular being venture capital, growth capital, leveraged buy-outs, distressed and mezzanine funding. In the end, GPs make strategic investments, restructure debt and provide management consulting to better position a private company to be sold either through IPO or privately, resulting in an attractive rate of return for the fund’s partners.

There are many different ways a private equity firm might structure a deal. For the purposes of this comparison we look at a leveraged buyout model.

This typically involves a firm/fund investing like this:

Analysts and partners research and target a distressed company

Target company has high growth potential but is burdened by debt

The company may or may not be on good organizational footing in terms of management

Growth is being muted by the inability to keep up with debt service, siphoning much needed cash to continue growing.

An injection of capital, a restructuring of debt and expert counsel on management will allow the business to get over the hump and grow. In exchange of course for this shot of life, the company trades equity and puts up collateral (factories, real estate, IP, etc.) to the PE firm and banks.

In theory, the PE firm is a great partner, they win if you win, but they also win if you lose and can sell off what’s left, earning back their investment at a minimum. This is where some of the scrutiny of the PE model has come into focus over the last decade as short-term financial gain often comes into conflict with the long-term strategy of their portfolio companies.

The leveraged philanthropic outcome (LPO) model (simplified)

By applying the same principles of PE to philanthropy there is opportunity for bold philanthropic investment in a distressed nonprofit market. Similar to PE target companies, there are many organizations with growth potential (measured in solutions and impact). Yet, they lack the necessary capital or have been racked with challenges (pandemic, management and debt) and could benefit from this type of strategic investment.

Much like a PE fund targets a specific industry, an LPO fund should focus on the strengths and network of its GPs. In philanthropy, this can be broken into similar sectors: poverty, water, education, housing, environment among many others. And while a PE fund is focused on a targeted rate of return (e.g. 15%-20%), the LPO must also focus on a metric for success, not only for its targeted investment (the organization) but for its investors (LPs).

The Fund

Like PE, these philanthropic funds should have a diverse set of stakeholders. But while LPs in a typical private equity fund may all have similar goals in their investment outcomes, an LPO fund brings together investors with very different motivations. This is a strength that the LPO has over PE in structuring their investments in targeted portfolio companies. LPOs could raise funds from the following entities, each with very different expectations in their investing approach, albeit adding complexity to the deal:

Foundations (Large, Small, Families, Corporations)

Investment philosophy: Pure philanthropy (negative 100%), No interest loan (0%), Low interest loan (2%-5%), High impact (metrics for successful outcomes)

Impact investors (Institutional, Venture philanthropists)

Investment philosophy: No interest loan (0%), Low interest loan (2%-5%), Venture capital (if connected to a social/environmental spinoff)

Individuals

Investment philosophy: Pure philanthropy, grants (negative 100%), Tax incentive, High impact (metrics for successful outcomes)

Traditional investors (Banks, CDFI, Institutional)

Low interest loans, market rate loans

These diverse LPs will allow the fund to deploy blended financial principles to make their investments. This could be compared to a mezzanine capital investment in private equity where some higher risk investors are prioritized in debt repayment in exchange for higher returns. By blending all of these investment outcomes and strapping them to a dependent, measurable outcome for an organization (e.g. building twenty-five houses for the homeless in a given timeframe) there is an ability to spread the risk and lower interest on debt for the organization, increasing efficiencies and freeing up capital.

And as with PE, the LPO fund should also provide an expert level of consulting for the non-profit and in some cases, occupy a board seat for a determined amount of time (until “exit/outcomes achieved”) to provide counsel and strategy. Again, in theory, this is a win-win for the organization as it gains the necessary investment it needs to survive and a seasoned expert to counsel them on strategic decisions for ultimate growth and impact.

Generosity must get aggressive

A strategy from the PE playbook that philanthropy must adopt is the aggressive targeting of potential portfolio investments. PE firms deploy an army of analysts, deal makers and consultants to find companies that meet their investment criteria. LPO funds should consider this approach, creating a pipeline of opportunities to make the most impact and generate the desired returns of their LPs. This would be a dramatic shift as most blended financial investments involving venture philanthropists are deal centric, rather than fund centric. Meaning, their investments are ad-hoc as deals arise, rather than pooling their funds with other like minded investors and allowing the GPs to go out and source these maximum impact outcomes. In short, a fund should invest in many nonprofits rather than wait to build a unique fund for each deal.

But where will these new funds find limited partners to invest?

One area could be the pile of cash sitting in donor advised funds. But as a recent Stanford Social Innovation Review article reveals, the root cause could be bigger than that.

A Bridgespan Group analysis discussed the famous Buffett-Gates Giving Pledge, where in the US alone, 140 Billionaires have signed on to give away half of their fortune. However:

Despite such aspirations, our analysis shows that ultra-wealthy American families donated just 1.2% of their assets to charity in 2017. That falls considerably short of average, long-term investment returns on assets. Compare 1.2% to the S&P 500’s 20-year, average annual returns of 9%, for example. The clear-eyed math shows that if an ultra-wealthy family wanted to spend down half its wealth in a 20-year time frame, the family would need to donate more than 11% of its assets per year—a tenfold increase over average current levels of giving.

As Jeffrey Walker, a veteran of PE and chairman of New Profit, a pioneer of the PE model for philanthropy concept points out:

The Forbes Billionaire list shows 2,153 billionaires from 72 countries have a total net worth of about $8.7 trillion. If they gave away 10 percent of those assets annually, the flow of funds would total $870 billion a year. Contrast this with the Bridgespan giving rate figure mentioned above of 1.2 percent which results in $104 billion of giving a year. How can we bridge this $766 billion giving gap?

Measurement is the key

The linchpin of this new philanthropic tool is measuring what matters. The nucleus of this comparison comes into conflict here -- but in the end, it will be the outcomes that matter to each investor. In a LBO, it will always be money. In the LPO, a blend of money plus impact. The attention to the design of this metric cannot be understated. The retention of an independent auditor would ensure a measurable framework by which investment impact could be defined and indexed. This binding tool will be critical and helps set the desired targets and predetermined methods to gather data as part of the deal. This has largely been an academic endeavor by scientists and research labs with direct expertise in the areas of impact.

While financial investing is guided by standardized frameworks like credit ratings and S&P benchmarks, there is growing concern by the industry to address this pivotal issue of ‘measuring the impact’ of philanthropy. Luckily some new tools and technology are being used more widely as an accepted way to deliver a return on investment.

Three examples:

The Science Based Targets Initiative (SBTI) helps companies transition to a low-carbon economic profile by setting greenhouse gas emission reduction targets in line with climate science. An initiative of the World Resources Institute (WRI) and funded by the Macarthur Foundation.

The Sustainable Development Goals (SDGs) or Global Goals are a collection of 17 interlinked goals designed to be a "blueprint to achieve a better and more sustainable future for all". The SDGs were set in 2015 by the United Nations General Assembly and are intended to be achieved by the year 2030.

The Global Reporting Initiative (known as GRI) is an international independent standards organization that helps businesses, governments and other organizations understand and communicate their impacts on issues such as climate change, human rights and corruption.

A new way of doing things

Operating a business versus operating a nonprofit is like chalk and cheese. But, much like a corporation, non-profits do have a binding fiscal responsibility to operate within their means. They must make strategic investments, tackle unmet problems otherwise left to society, create compelling solutions (a product) and recruit and retain the best talent to fulfill on this mission. Like with any business, this will ultimately determine if investors (donors) will fund the endeavor. More importantly, sound execution creates a recurring revenue stream of support (sales) therefore continuing the flywheel and solving these important societal issues. And while businesses will measure success in profits and shareholder value, nonprofits will measure success in impact and, if successful, a diminished reason to even operate.

Imagine a business saying, if we hit all of our goals, we will go out of business! But in its purest form, this is the ultimate measurement of success for a nonprofit.

In short, much like a struggling company with a profitable idea, they need help and they need unrestricted capital.

As Rory Sutherland points out in his recent book Alchemy:

Alongside the inarguably valuable products of science and logic, there are also hundreds of seemingly irrational solutions to human problems just waiting to be discovered, if only we dare to abandon standard-issue, naïve logic in the search for answers

Leveraged Philanthropic Outcomes could be the answer.

More on private equity, philanthropy and doing things differently:

Emily Stewart does a great job explaining the basics (and perils) of private equity and leveraged buyouts here.

SPACs are all the rage right now. Can there also be lessons for philanthropy in this hot investment tool? Recently some giant private equity firms, Dyal and Owl Rock announced they would join forces, invest in other private equity firms and then seek acquisition through an SPAC. More on this interesting development here.

Philanthropy and venture capital in conversation with each other. Knight Foundation CEO Alberto Ibargüen and Venture Capitalist Austin Clements offer perspectives in this episode of the Off the Sidelines podcast.

File this under thinking differently. Maine is exploring growing fish indoors. US inland farms offer an alternative to diminishing wild Atlantic stocks, but the price tag is bigger carbon emissions - more here from The Guardian.

Special thanks to my friends at @beondeck: Stacy Ndlovu, Tom White, Anant Kapoor, and Shawn Lestage. I learned a lot from the National Council on Nonprofits and as mentioned above, some of the pioneers of innovative financing in philanthropy Jeffrey C Walker and New Profit

I was also inspired to revisit this topic while reading another substack this past week by Mark Tercek called The Instigator. (Which I highly recommend). He illuminates a great opportunity for measurable climate action (moving the needle type stuff) within the private equity space. Which got me thinking about private equity again….

You are receiving this email because you signed up for Interior Analytics, a newsletter about the business of American nature. I cover topics ranging from national parks and science to business, policy and technology. If you are new here or someone shared this with you, welcome! Poke around my other posts and if you like what you see please subscribe.

Oh, and hit the like button. You know, if you liked it.